This article is the onsite version of the Unhedged newsletter.sign up here Send newsletters straight to your inbox on weekdays

good morning. I woke up early yesterday morning and was afraid to look at my phone. I didn’t want to know what the Credit Suisse stock price was. When I looked into it with one eye, it got bigger and I went to sleep again. When I woke up for the second time, I was again relieved to see the US Banking Index going up, and all but First Republic had gone down significantly. This story keeps coming up. Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

First Republic (and banking system)

As of yesterday morning, First Republic’s stock has fallen 80% in just over a week. First Republic continued to fall even as other local bank stocks recovered. However, it turns out that the bank has some important friends.from lunch at the bank press release:

Bank of the First Republic. . . today, March 16, 2023, from Bank of America, Citigroup, JP Morgan Chase, Wells Fargo, Goldman Sachs, Morgan Stanley, Bank of New York Mellon, PNC Bank, State Street, Trist and U.S. Bank. announced that it will receive a total of $30 billion in uninsured deposits. .

This seems to have helped a bit. Stocks ended the day with him up 10%. But it’s worth noting that the stock, which was at $115 last week, is now at $34. As of this writing, banks are down another 18% in aftermarket trading (often thin and unrepresentative, but still). Why didn’t it have a lasting effect? I don’t know. Some possibilities:

-

At the end of the fourth quarter, First Republic had $176 billion in deposits. If depositors are horrified by the stock price, why not fill the void with $30 billion?

-

The 11 depository banks have $1.2 trillion in equity and $14.1 trillion in assets. Did $30 billion seem a little out of the way?

-

First Republic has declared it has $34 billion in cash, in addition to the $30 billion it just deposited. But he also revealed that in the past week he has borrowed $109 billion from the Federal Reserve and added $10 billion in new loans from the Federal Home Loan Bank (more on that later). I will explain). Again, how big is the hole we’re trying to fill here?

-

The bank said insured deposits have remained stable since the problems began on March 8. However, the market for uninsured deposits, which stood at $119 billion at year-end, or 67% of the total, was not renewed.

But who really knows. Everyone is nervous. You don’t need a good reason for a stock to go down.

A question that can be answered a little more substantively is why the stock market chose the First Republic in the first place. Guaranteed deposits made up just 3% of SVB’s total. Long-term bonds were 55% of his SVB assets, compared to 15% for the First Republic. Even if the unrealized losses on these bonds were to materialize, it wouldn’t have taken a huge toll on First Republic’s stock. well?

Part of the answer was clear to everyone from the beginning. First Republic, which is essentially a bank for the wealthy, has a huge amount of mortgages on its balance sheet, representing about half of its total assets. They have the same unpleasant characteristics of SVB securities: they have low yields (less than 3%) and remain low even as interest rates rise and the cost of First Republic deposits rises. This is bad.

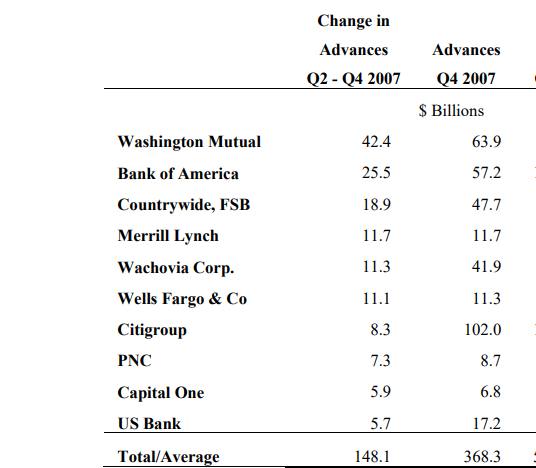

But there is another, more important reason for market penalties. It has to do with small items on the liability side of the balance sheet: loans from FHLB, or “advance payments.” By the end of 2022, it will total $14 billion. A year ago, that total was just $3.7 billion.

The reason this is relevant is because FHLB is where banks go when they need funding for whatever reason. The history of the 11 regional FHLBs is a topic in itself, but important to our purposes is that they lend to other member banks, using government bonds and other assets as collateral. FHLB is funded by issuing bonds with an implied guarantee from the US government. As of December, FHLB had total assets of $1.2 trillion. Importantly, if the bank they lend to fails, they will be the first creditor, before the Federal Deposit Insurance Corporation.

Directed by Aaron Klein of the Brookings Institution (read his excellent work on FHLB. here and here), we’ve seen Q3 filing For the San Francisco FHLB, see who the largest borrowers are. Interesting group:

SVB number one. The first Republic Two and another recent target in the market, the Western Alliance, took his fourth spot. Then I took Klein’s advice and looked into the New York Fed. paper About FHLB, “The FHLB System: One Lender to Another?” 3 of the top 5 no longer exist.

Increasing FHLB loans is “a classic red flag that distressed financial institutions are borrowing more,” says Klein. I can’t say exactly why First Republic needed the cash, but they needed it. Klein is surprised that the SVB supervisor didn’t pay attention. “SVB failed a remedial test and the regulator gave him an A,” he says. Equity investors didn’t seem so generous. They may have seen his SVB problem and sorted banks by FHLB loan increases and made deals accordingly.

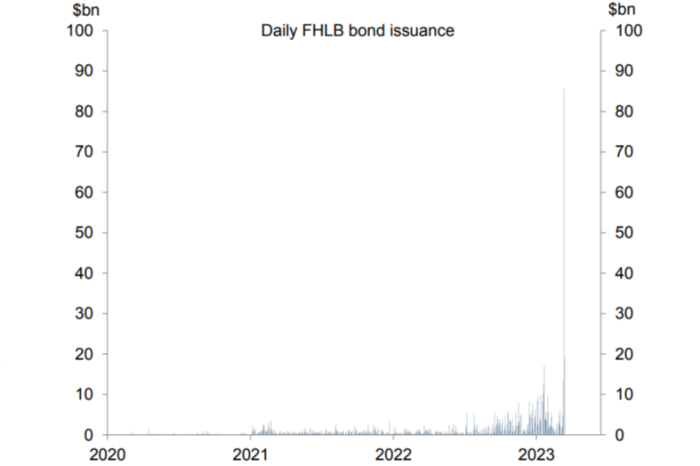

So who is currently borrowing from FHLB? Banks seem to be the majority. FHLB borrowing cannot be tracked in real time, Disclosure Proprietary bond issuance as an indicator of borrowing levels. Jan Hatzius’ team at Goldman Sachs provides this chart, which shows issuance surpassing his $80 billion in the past few days.

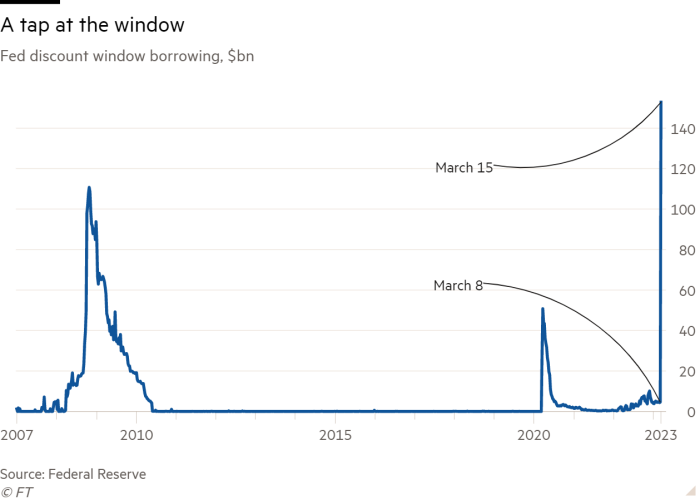

This does not mean that many other banks have the same kind of problems as SVB and First Republic. Instead, either the SVB turmoil has scared them into being cautious, or depositors are withdrawing their deposits – simply out of blind fear – that all banks are getting as much cash as possible. could mean We are generally in a banking panic, albeit mild so far. And it’s not just his FHLB that banks want cash for. They borrowed $5 billion from the Fed’s discount window for the week ending March 8. Last week it was $152 billion, more than any other week during the financial crisis.

To emphasize, this chart shows a lot of fear, not a lot of bankruptcy. But when depositors withdraw cash from the banking system, where does it go? Partly to money market funds. The FT reports net inflows into money market funds. Reached $120 billion Over the past week, it hit its highest level since mid-2020. From the FT story:

The US financial system is very nervous right now. Strange things are likely to happen.

one good read

Ron DeSantis sorely wrong About Ukraine, economists argue.

https://www.ft.com/content/9869c0f7-24f6-43c3-b8d3-b0d884f402fc Red Flags of the First Republic | Financial Times

- Los Angeles County’s Struggling Juvenile Halls Granted Extension, Allowed to Remain Operational Following Enhancements

-

-

-